Nic Carter's Bogus Reporting on Silvergate Bank

Wave examines Nic Carter's false and misleading reporting on the demise of Silvergate Bank. Plus: Ryan Salame's bombshell alleges Silvergate directed the fraud at the heart of the FTX bankruptcy.

Venture capitalist Nic Carter says that Silvergate Bank was “opportunistically executed amid the fog of war during the 2023 banking crisis, as part of a broader coordinated attempt to de-bank the crypto industry.”

Carter’s faulty reporting first caught my attention in September 2024 when he published a thread on X claiming that Silvergate Bank was a victim of a political conspiracy which he branded “Operation Chokepoint 2.0.”

Carter contends that short seller Marc Cohodes conspired with United States Senator Elizabeth Warren to encourage “a bank run, based on rumors that silvergate had criminal exposure to FTX (they have since been totally cleared of those allegations).”

His pronouncement struck me as an outright falsehood. There are no legal processes which have “cleared” Silvergate of its "criminal exposure to FTX.”

I messaged him, asking to explain and provide evidence to support his claim that Silvergate Bank was "totally cleared of those allegations" of "criminal exposure to FTX.”

“I mean what I wrote, feel free to refer to my tweet,” Carter replied.

“To my knowledge, ‘criminal exposure’ is a pretty loose term without a specific legal definition. Do you mean exposure to the criminal activity of FTX?” I responded. “Who cleared Silvergate of such allegations? How?”

“Not debating you. You know what I mean,” he wrote back, and promptly blocked me.

Despite receiving a block, I reached out to Carter via e-mail prior to publication of this story. Some of his responses are included throughout this article.

Carter has variously referred to Silvergate’s voluntary liquidation as an “execution” or a “murder,” but these violent metaphors are completely disconnected from the reality of what went down between Silvergate and FTX. I believe it is more likely that the self-liquidation was a tactic to avoid further action from federal regulators.

Carter worked overtime during these past few months to steer the dialogue around Silvergate’s demise, appearing on podcasts and publishing writing at multiple outlets. His work circulated and marinated on social media without much pushback, until a16z’s Marc Andreessen appeared on Joe Rogan’s show and proposed a corollary argument originating from Carter’s reporting. The interview made waves across social media, with many popular commenters criticizing Andreessen’s remarks about the Consumer Financial Protection Bureau.

Yet, no one has returned to appraise the root of the conversation. At the nucleus of the debanking argument is Carter’s proposal that Silvergate “had been unjustly forced to liquidate or shuttered due to this anti-crypto animus in the government.”

Evidence demonstrates that this claim is false. Carter has been advancing a highly misleading narrative which casts Silvergate as a victim.

But Silvergate is not a victim. They were complicit in — and perhaps even culpable for — FTX’s criminal activity.

Silvergate and the Heart of the FTX Matter

FTX was Silvergate’s most important customer. By the time of FTX’s implosion in November 2022, FTX entities reportedly held over $2 billion in deposits at Silvergate, composing 17% of Silvergate’s overall deposits. The presence of FTX helped drive explosive growth of Silvergate’s assets, which increased from less than $1 billion in 2017 to more than $16 billion by the end of 2021.

Former FTX CEO Sam Bankman-Fried proclaimed that Silvergate “revolutionized banking for blockchain companies,” a quote featured prominently on Silvergate’s website.

Silvergate’s premier product was the “Silvergate Exchange Network,” known as “SEN.”

SEN enabled Silvergate customers to make near instantaneous US dollar transfers from one account to another on a 24/7 basis. This product was attractive to cryptocurrency firms and exchanges for its unique payment settlement capability, and many prominent crypto companies quickly made a home at Silvergate in order to make use of this powerful network.

Alameda Research, founded by Sam Bankman-Fried, joined Silvergate as a customer in 2018. FTX, the crypto exchange founded by Bankman-Fried, followed a few years later. As FTX’s involvement with Silvergate grew, so did SEN: dollars transferred over SEN increased by over twentyfold from 2019 to 2021.

The most essential fact to know is that Silvergate hosted the FTX-Alameda-North Dimension banking nexus. This scheme facilitated the transfer for FTX customer funds to Alameda’s bank accounts at Silvergate. FTX customers were directed to wire their funds to an entity called North Dimension, a fake online electronics retailer. Alameda transferred customer funds from those Silvergate-hosted bank accounts and spent the money or invested those funds — personal property which belonged to FTX’s customers.

The fraud at the heart of the FTX bankruptcy transpired thanks to the decisions of Silvergate’s executives, including former CEO Alan Lane.

Nic Carter’s Inaccuracies, Distortions, and Omissions

A couple weeks after Carter’s Silvergate thread in early September, he published an article at Pirate Wires expounding on his perspective.

There are many inaccurate and misleading details scattered throughout the piece, but Carter made a serious error by severely downplaying Silvergate’s failure to monitor over $1 trillion in transactions on SEN. He wrote:

“The actual issue, I discovered, was that Silvergate’s transaction monitoring system for SEN had gone through an upgrade and experienced an outage. Because SEN was a settlement network for Silvergate’s own clients, every transaction on SEN was between clients known to the bank that had gone through rigorous KYC (Know Your Customer) and onboarding processes. So even during the monitoring outage, it’s not like the transactions were between unknown firms.”

This paragraph is a full-throated lie. Extensive evidence provided in the SEC’s complaint against Silvergate and employee statements (via a class action lawsuit) expose the faults in Carter’s “reporting.” The issue was not merely an “outage,” and during this so-called “outage” there were no “rigorous” KYC or onboarding processes, and transactions frequently occurred on SEN between parties unknown to Silvergate.

For at least 15 months, transactions on SEN went unmonitored because senior leadership failed to implement anti-money laundering (AML) software which would have detected suspicious activity. More than $1 trillion in SEN transactions did not receive automated monitoring between April 2021 and September 2022.

The new software was introduced in April 2021 to meet Silvergate’s internal policies for intelligence-based surveillance, which was necessary to monitor billions of dollars transferred by cryptocurrency industry clients and maintain compliance with the Bank Secrecy Act (BSA).

Silvergate’s BSA officer communicated to bank Chief Operating Officer Kathleen Fraher in January 2022 that there were issues with the new software, writing to Fraher that their new automated transaction monitoring system “can’t take SEN transactions [into] consideration for risk rating purposes.”

Fraher responded: “We have known of this issue and either we have established other controls to account for it or we haven’t and we have to take our lumps.”

Nine months later, Silvergate’s BSA staff prepared and shared a report with Fraher which concluded that their new software had not been monitoring SEN transactions in a manner that would help identify suspicious activity or provide adequate ongoing monitoring.

The Gates Were Open

Meanwhile, Alan Lane and his executives were lying through their teeth about Silvergate’s regulatory compliance commitments to shareholders, to the public, to bank examiners, and to Congress. Just a few of many examples include:

Silvergate’s 2021 Form 10-K, which stated that Silvergate “developed enhanced procedures to screen and monitor these customers, which include … a system of “red flags” specific to various customer types and activities … [to] adequately screen and monitor our customers associated with the digital currency initiative for their compliance with anti-money laundering laws.”

Lane’s statements In a June 2022 CNBC interview: “As a regulated financial institution, Silvergate complies, obviously, with all of the federal and state regulations and we essentially need our customers – we require them to comply as well. And so we only bank institutions who are also serious about regulations, so, ironically, we actually welcome [increased scrutiny].”

Lane’s letter (reviewed and approved by Fraher) about risk management published November 21, 2022: “Silvergate conducted significant due diligence on FTX and its related entities, including Alameda Research, both during the onboarding process and through ongoing monitoring, in accordance with our risk management policies and procedures and the requirements outlined above.”

Lane’s December 19, 2022 response to an inquiry from Congress: “In compliance with the Bank Secrecy Act and the USA PATRIOT Act, we determine the beneficial owner, the source of funds, and the purpose and expected use of funds for each and every account we open. Silvergate also monitors transaction activity for every account and identifies activity outside of the expected usage. When we

identify certain kinds of activity, we are required to confidentially file suspicious activity reports, and we do so routinely. We have a track record of closing accounts that are used for purposes outside of their expected use.”

Extensive accounts provided by former Silvergate employees in a class action lawsuit underscore that Lane’s statements are flagrant lies or false representations.

One former senior vice president at Silvergate stated that the bank did not vet existing customers before adding them to the SEN Network. The SVP, who started at and departed Silvergate in 2019, stated that she did not see efforts by Silvergate to know their customers or ensure legal compliance. Instead, she said their focus was on sales and client acquisition, especially following the turn towards crypto clients.

The former senior VP confirmed that she “never heard of Silvergate conducting any of the specific onboarding measures that Lane and Silvergate had claimed repeatedly to customers and investors that they performed.”

Once customers got access to SEN, there was a glaring absence of ongoing monitoring. There was no AML alert monitoring, no daily news reviews, no quarterly account activity reviews, and no training for employees on how to conduct monitoring that could have helped detect illicit activity.

Another former Silvergate employee who worked as a BSA analyst from 2017 to 2019 stated that about half of Silvergate’s customers were unknown to the bank. His understanding was that Silvergate would bank anyone who wanted to be a customer. He “reported that he and his fellow analysts felt like they were checking boxes for the sake of it without the Bank actually being mindful of the risk they were absorbing.”

The BSA analyst said that everyone in his department raised compliance concerns to their manager “regarding customers they believed should be exited but would not be by order of Silvergate’s Chief Operating Officer.” (Fraher was COO from 2018 to 2022, overlapping this period.)

The BSA analyst further claimed that suspicious activity reports were absorbed and justified as an effort to preserve business relationships. No Silvergate customer accounts were ever closed, he said. Other former employees attested to the same, with one manager saying that the bank never declined a client, and that there was no record of a prospective client ever being denied approval.

A former VP of Deposit Operations (employed at Silvergate from 2011 to 2021) stated that Silvergate failed to investigate reports from customers and other banks about unauthorized transactions. The VP also explained that in 2018, Silvergate started receiving ten to twenty subpoenas per month from the U.S. Attorney’s office. These subpoenas concerned incoming customer wires – including incoming wires for Alameda.

A digital banking manager who worked at Silvergate from March 2022 through November 2022 also challenges Lane’s narratives. This manager was responsible for the SEN, including onboarding. The procedures Lane references in the quotes above did not exist, per her recollection.

The manager explained that when customers wanted to join SEN, “the gates were open.”

When it came to SEN, there was no due diligence, no compliance research, no anomaly detection, no wire limit requirements, and no reviews or approvals from management, according to this manager. When she sought out KYC and beneficial policies on Silvergate’s intranet, she was unable to locate procedures concerning compliance. The AML software purchased by Silvergate was never implemented.

She recalled a conversation with her manager, Dina Matias, in which she questioned why a $250 million wire limit was provided to a customer with only $70,000. Matias, who reported to Chief Administrative Officer Elaine Hetrick, screamed at the manager in response, per the manager’s recollection.

The banking manager also claimed that Silvergate employees were directed to complete beneficial ownership forms on behalf of the clients. This allegation is corroborated by a former Silvergate client manager, who confirmed that at the direction of Silvergate management, he and other relationships managers completed beneficial ownership paperwork for both new and existing clients.

Beneficial ownership information helps the Financial Crimes Enforcement Network identify who owns or controls a company. Since only the companies themselves can provide accurate ownership information with absolute certainty, it would be both unusual and inappropriate for Silvergate relationship managers to complete BOI forms on behalf of their customers.

Silvergate had also represented to investors that they performed site visits as part of their compliance reviews, which are inspections that help a bank assess the legitimacy of prospective clients’ business operations. Site visits can be an important step to help prevent money laundering and ensure that shell companies aren’t abusing the bank, as in the case of North Dimension.

Four of the aforementioned employees stated that Silvergate did not conduct site visits.

I asked Carter why his reporting failed to mention the extensive and troubling details shared by Silvergate’s former employees.

“Don’t have a view here,” he responded. “I’m not conducting a forensic investigation of silvergate, I’m writing about bank regulatory policy.”

Matters Requiring (Immediate) Attention

One of Silvergate’s former due diligence managers (employed from May 2022 to May 2023) said that the Federal Reserve reportedly sent Silvergate a report identifying Matters Requiring Immediate Attention (known as “MRIAs”) pertaining to their client vetting, due diligence, and onboarding practices. Regulators apparently also identified deficiencies with Silvergate’s ongoing monitoring procedures and suspicious activity reports.

“Virtually every bank examination includes some nominal ‘matters requiring attention,’ as there are always areas for improvement,” Carter wrote in his Pirate Wires piece. “Regarding Silvergate’s failure to detect FTX’s various schemes, banks are not expected to catch every single instance of suspicious activity among their clients.”

Carter’s source appears to either misconstrue or misunderstand this particular action from the Federal Reserve. He claims that a source with knowledge of the situation tells him the examinations resulted in MRAs, as opposed to MRIAs.

The Federal Reserve makes an important distinction between MRIAs and MRAs, the latter of which Carter is referencing.

Via his e-mail response, Carter told me that he was “not familiar with the distinction” between MRAs and MRIAs. The nature, urgency, severity, and threat to organizational safety and soundness are what distinguishes the two categories. When Federal Reserve examiners issue MRIAs, the organization is required to take immediate action, whereas MRAs provide longer time frames.1

When regulators returned to check Silvergate’s progress in June 2022, the MRIAs were going to remain in place, according to the due diligence manager. He believed Silvergate would receive even more MRIAs.

In response to the Federal Reserve, the manager and his team created a new set of procedures to be implemented in August 2022. Prior to this time, he says Silvergate did not evaluate the compliance culture of prospective clients during the onboarding phase. Reviewing previous records, he could not discern customer identities, their jurisdictions or sources of wealth, or a traceable flow of funding.

Once the new set of procedures was rolled out, the due diligence manager wanted to re-review any customers who were not vetted by the new onboarding process, as per industry standards. His supervisor agreed with the recommendation.

Silvergate did not follow his recommendation, he said.

Regardless of the veracity of these statements from former employees, Lane knew that Silvergate’s regulatory compliance program had critical deficiencies after multiple bank examinations which found serious flaws in the bank’s transaction monitoring systems.

Instead, he chose to misrepresent the truth in order to hide deficiencies in Silvergate’s BSA program from investors, while reportedly unloading over $21 million in Silvergate stock over the years.

Too Little, Too Late

Silvergate’s failure to monitor FTX and Alameda was a deliberate choice. It was almost like the executives deliberately turned a blind eye, knowing that crime would inevitably fester within their walls, but also knowing that conscious neglect would help attract valuable clients who intended to conduct illicit business. In the end, willful ignorance brought in more clients and more volume, which meant more opportunities to line their own pockets.

After FTX filed for bankruptcy, a Silvergate board member requested that the bank review its relationship with FTX. Lane brought this request to Fraher, and Fraher told him that she had already ordered the BSA staff to review FTX’s activities through Silvergate.

Less than one week after FTX filed bankruptcy, Silvergate staff identified about $9 billion in suspicious transfers related to FTX’s entities.

“Most troubling to the BSA staff was the trend of funds that flowed from FTX’s custodial accounts—which held FTX customer funds—to a series of non-custodial FTX-related entities’ accounts, followed by transfers of these funds to other third parties—either through the SEN or to accounts external to the Bank,” reads the SEC complaint.

Silvergate finally decided to have a look after it was too late, and it took less than a week to identify the source of the problem. Yet, I don’t think they even needed more than one day. If executives and management spent even a few hours investigating the FTX matter, they likely would have quickly identified illegal activity. A smidge of effort could have mitigated the carnage that followed FTX’s collapse.

Ryan Salame’s Bombshell

Former FTX and Alameda executive Ryan Salame alleges that Silvergate executives and lawyers actually advised and directed the whole operation.

In summer 2024, Salame repeatedly asserted that Silvergate directed all of Alameda and FTX’s banking activity. He said this was done at the behest of Silvergate executives.

“Silvergate instructed alameda / [North Dimension] to use their accounts while they figured out a solution internally (as a bank) how to onboard ftx [sic] directly. Lawyers / executives / everything,” reads one of Salame’s many posts about Silvergate.

If Salame’s allegations have merit, that would mean that Silvergate was not just complicit, but directly orchestrated the facilitation of FTX customer funds into Alameda’s coffers.

In the Bankman-Fried sentencing memorandum, the government states that Silvergate communicated that it would not open an account to facilitate FTX customer deposits unless FTX could show that it was licensed and registered as a money services business. To maneuver around this restriction, Alameda employees submitted a falsified application to Silvergate stating that the purpose of the newly incorporated North Dimension was for trading and market making and that North Dimension was not a money services business.

Silvergate approved North Dimension’s bank account application in April 2021 — the same month in which the bank stopped monitoring SEN’s transactions. The North Dimension Silvergate bank account ultimately processed billions of dollars worth of transactions over the course of at least 9 months.

What is unclear is why Silvergate would be supposedly so firm as to ensure that FTX abided by the law and regulations initially, then abruptly and utterly neglected to exercise even the most basic due diligence. North Dimension wasn’t a mystery: it had no employees or real business operations. Their website clearly showed they had nothing to do with crypto trading or market making, contrary to the application Silvergate approved. The company was registered at the same address as FTX US. The prices of the electronics were nonsensical, and there was no viable way to actually order anything from the shoddy, typo-ridden website.

Nor was any of this a secret to Silvergate. FTX publicly displayed instructions for customers to wire their deposit funds to North Dimension. Silvergate did not need to do any serious or in-depth investigatory work — any user with an FTX account who went to deposit funds during this period would have seen these instructions.

On top of all of these glaring red flags, Salame further claimed in a July 2024 post on X that Alameda (and later, North Dimension) had thousands of incoming and outgoing wires with “FTX” written in the wire reference field.

The bank had a litany of opportunities to easily and quickly analyze the activities of the bizarre shell company of its most vital customer, yet for some reason it chose to look the other way.

The notion that Silvergate did not know what FTX was up to with their North Dimension account exceeds the boundaries of plausibility. The only reason I can fathom that this travesty was permitted to unfold is precisely because the Silvergate executives wanted it to happen — likely because it was good for their own personal bank accounts.

While there is a good argument here to be made about regulatory failure in regards to Silvergate,2 it is not the misinformed argument being pushed by Carter.

The Secret Sauce

Lane once bragged in an interview that “our compliance and due diligence is our secret sauce.”

Yet, Silvergate’s real secret sauce had nothing to do with their compliance or due diligence procedures. Lane’s true secret sauce? Nepotism, which played a major role in his bank’s downfall.

Alan Lane’s son, Chris Lane, as well as two of his sons-in-law, served in executive positions at Silvergate. Until November 2022, Lane’s son-in-law, Tyler Pearson, served as Silvergate’s Chief Risk Officer until November 2022. Another son-in-law of Lane, Jason Brenier, held several positions at Silvergate starting in 2018, including senior VP positions which give him purview over correspondent banking and client relationship management.

These men were in positions to make critical decisions which ultimately impacted the tumultuous outcomes of Silvergate and FTX.

As the Office of Inspector General phrased it in their summary report: “Silvergate’s board of directors and senior management were ineffective … Further, nepotism, evidenced in the several familial relationships among members of the bank’s senior leadership team, undermined the effectiveness of the bank’s risk management function.”

On the other hand, Carter does not seem to believe that nepotism was an issue of concern for Silvergate.

“I know people were critical of the Chris Lane hire but it doesn’t bother me too much,” Carter replied in response to my inquiry.

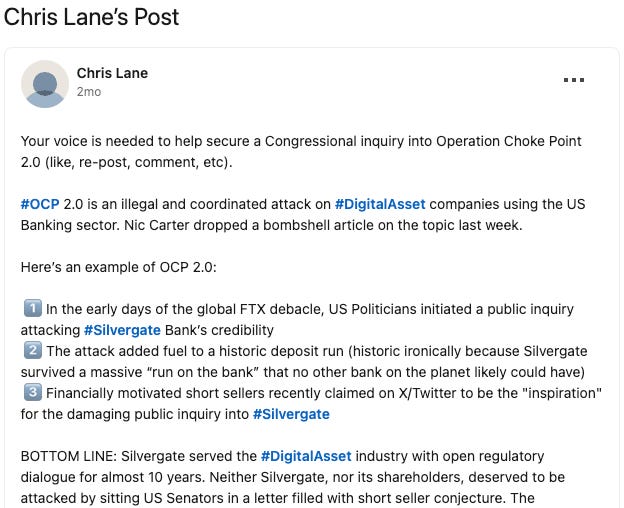

Alan Lane’s son, Chris Lane, appears to be circulating Carter’s work while claiming that “neither Silvergate, nor its shareholders, deserved to be attacked by sitting US Senators in a letter filled with short seller conjecture.”

Chris Lane’s post demonstrates a pathetic lack of remorse. Chris was arguably unfit to hold his senior positions as Silvergate’s Chief Technology Officer or as Chief Operations Officer. Given that technology and operational failures are at the core of the Silvergate debacle, Chris failed to uphold his duties and protect both the investors of his bank and the customer of FTX.

Why would Chris feel it is appropriate to pretend to be a victim?

Chris is complicit in the FTX bankruptcy. The truth about his daddy’s bank is that it grossly mishandled the money of working class individuals, and Silvergate’s neglect of their responsibilities created a devastating tragedy for people around the world.

FTX victims are real human beings who endured psychological trauma and profound disruptions to their personal lives. Families grappled with losing life savings, shattered dreams, and the threat of losing their homes. Children witnessed the lives of their parents become completely destabilized. Many victims struggled with severe depression, strained relationships with loved ones, or an inability to pay for medical expenses. Some pondered suicide.

“You have stolen a life from me,” reads one victim statement.

Whitewashing White Collar Crime

I myself lost money on FTX’s exchange when it collapsed. I do not care about getting my money back. Instead, I wish for the public to know the truth about what actually happened. And the truth here is that Silvergate Bank was a criminal hellhole of nepotism and corruption which facilitated the illegal activities of FTX and Alameda Research.

Carter’s reporting neglects to reference or wrestle with any of these details, possibly because they are inconvenient to his ideological arguments. His argument about Silvergate has been cast by supporters as journalism, but it is merely vapid corporate propaganda. He made up his mind about Silvergate long ago, and has ignored or dismissed new evidence that contradicts his beliefs.

Silvergate was not “killed” or “murdered” or “executed.” Carter’s framing of the Silvergate saga is a manipulative form of historical revisionism.

Venture capitalists like Nic Carter will not be allowed to whitewash the history of white collar crime without a fight.

MRIAs include “(1) matters that have the potential to pose significant risk to the safety and soundness of the banking organization; (2) matters that represent significant noncompliance with applicable laws or regulations; (3) repeat criticisms that have escalated in importance due to insufficient attention or inaction by the banking organization; and (4) in the case of consumer compliance examinations, matters that have the potential to cause significant consumer harm.” Additionally, MRAs have been issued with greater frequency over the years, and are less concerning than MRIAs.

If Carter’s source is accurate, and Silvergate received only MRAs, then his analysis is probably on target. But given the abundance of evidence about Silvergate’s behavior, it seems more likely that Silvergate’s due diligence manager is telling the truth about the Federal Reserve’s issuing actions which required immediate attention, whereas Carter’s source is minimizing or concealing the reality of the situation.

Notably, the attorney for Silvergate in the class action suit argued in December 2023: “we're not arguing – certainly, at this stage of the proceedings – that the former employees are lying. Or that they – that there is a factual dispute here.” This may lend further credence to the claim that Silvergate received MRIAs.

Namely, sluggish and ineffective corrective actions to address underlying problems. Arguably, if regulators deployed more aggressive action earlier, the damage of FTX could have been lessened.